If you’re starting a hostel or you’re already running a hostel, you inevitably come across this one dreaded topic: insurances. But are they really necessary? And if so, what kind of insurances do you need and how much do they cost?

Before we get into the nuts and bolts of hostel insurances, let me tell you why this is probably the most honest piece of advice you’ll ever likely to come across on this topic:

Not long ago, I was running my own financial consulting business. And guess what: a good financial plan is ALWAYS based on one solid foundation: insurances. Hence, I claim to know not just “a thing or two” about the topic.

Insurances have never been my favorite topic, even though this was the first thing I needed to talk about with my clients. And despite the fact that I’m officially a “certified independent insurance broker”, I had a very different approach to this.

In fact, I don’t know of any other insurance broker who actively told his clients that certain insurances are a waste of money and that it’s best to get rid of them as soon as possible.

My favorite subject was – and still is – investments. In other words: the process of making $2 out of $1.

Even though I’m still a financial consultant for some friends and acquaintances of mine, I only do this because I know the stuff and I know I can tremendously help people.

I gave up my financial consulting business as I stumbled upon a new and even greater passion of mine: hostels. You can read my full story here.

That all being said, I’m NOT an active financial consultant anymore. Please read my disclaimer at the bottom of this page.

So, without further ado, let’s dig into this exciting topic!

Hostel Insurances - Do You Really Need Them?

“Is no insurance an option?” or “Aren’t insurances a waste of money?” – I heard this sentence over and over again in different variations.

Especially when money is tight you might be wondering if you can cut your spendings on insurances to “save costs”, right? And you know what? – I can relate a 100%. I’ve been there.

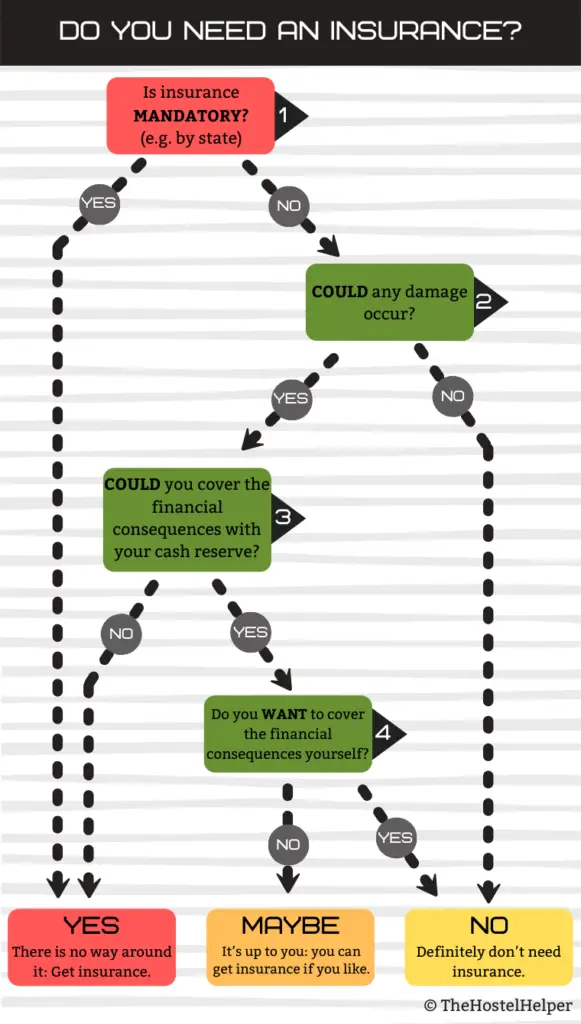

To clear up any bewilderment, I want to show you an easy 4-step process to make you able to figure it out yourself. Please be distinctly aware that the information that follows holds true for hostel insurances as well as insurances in your personal life.

This foolproof method was part of my consultation with clients and helped hundreds of people to save thousands of dollars each and every year.

Here’s what it looks like:

Alright. Let’s go through it step-by-step.

#1 Step: Is insurance mandatory?

The first thing you have to find out is if the insurance is mandatory or not. Unfortunately, there are not only different laws and rules for each country but also for each state and even city.

Hence, I recommend you do your own online research, ask nearby innkeepers or nearby lodging associations. They should have a wealth of information on the topic.

Obviously, if it’s mandatory, you do need one. No questions asked. DO NOT start your business without all compulsory insurances! This can backfire with high penalties that are calculated based on each day you weren’t insured.

#2 Step: Could any damage occur?

If the insurance is not mandatory, ask yourself if a damage is likely to happen or not. It’s important to note that it does NOT matter how high or low the probability of an event is.

None of us has a crystal ball to look into the future (…even though there are plenty of people who claim to have this skill). Hence, no matter how atomic the odds are, if a damage could happen, we need to act far-sighted and take responsibility while things are in order.

If it’s impossible to experience any damage, you obviously don’t need insurance. You’d be surprised how many policies I’ve seen for which people pay a premium voluntarily to cover issues that simply cannot happen.

Lastly, what about the scenario when you haven’t had insurance for 10 years and nothing ever happened? Unfortunately, in this case, the past doesn’t predict your future the slightest bit.

When it comes to finances in general, one of the most important aspects is to be able to look at things from an objective and rational standpoint. Don’t let your emotions take control here, no matter how hard it might seem.

This can result in the difference between losing 40% of your hard-earned retirement funds or almost doubling your money within a few years as we’ve seen during the last financial crisis in 2009.

#3 Step: Can you cover the financial consequences with your cash reserve?

Having a cash reserve is what I recommend not only for your business but also for your personal finances. A cash reserve is an instant accessible – also called “liquid” – pot of money. This could be as simple as cash or a checking account.

A good rule of thumb is 3-6 x your monthly operation costs. This ensures that even if the worst case were to happen, you would still be able to operate your hostel.

Nate Bunger, manager of the “Casa Miraflores” hostel and author of “How to Start a Thriving Hostel and Retire in Paradise” (recommended read), experienced first-hand how crucial a cash reserve is.

He went through an extreme dry season of 7 months without rainfall. Hence, the city lake was almost dried up and the water company had to shut down the water supply system to save water.

Guests obviously complained about not having water and the entire tourism in Colombia started to slow down. Fortunately, he had a big enough cash reserve to stay in business.

Okay, back to the initial question.

If you’re able to cover the financial consequences yourself, you do not necessarily need insurance. For this purpose, try to imagine what the worst case would be and how much it would cost you.

What might sound trivial, explains the counterintuitive fact that rich people need fewer insurances than poor people.

Think about it.

If you were a billionaire and one of your houses completely burned down, how much of your cash reserve would be effected? Well, if you weren’t insured, this would definitely hurt. But it certainly wouldn’t ruin you, right?

How about the next scenario: you’re a young entrepreneur, bought a $500.000 building on credit and before you’re opening the doors an explosion destroys the entire building. Unfortunately, you didn’t have insurance. How will this event change your life?

The bottom line:

Cutting down on insurances when the money is tight is the WORST thing you could do. That’s the moment when you need them most.

If the potential financial consequences are higher than your cash reserve, you HAVE TO insure yourself. Otherwise, it could affect your life dramatically and even RUIN you.

Hence, I personally call insurances of this category the “must-have insurances”.

#4 Step: Do you want to cover the financial consequences yourself?

Finally, if your financial reserve is larger than the potential damage, you’ll have to ask yourself if you WANT to pay that money in case something happens.

In this case, there’s no right or wrong. Some people have a higher need for safety, some don’t. This is often called “risk tolerance”.

I personally belong to the category of people who have a minimal need for safety. Hence, I only have must-have insurances for myself and go along the principle:

- TheHostelHelper

I also don’t believe in Murphy’s law: “Anything that can go wrong will go wrong”. Instead, I believe in the principle that there’s a reason behind everything that happens to me. And there will come a day when I find out what it was – even it if takes years (e.g. the death of my mother when I was 9 years old).

I personally am convinced that the universe with its accompanying laws will give me answers when the time is right. But back to our insurance topic. You might be a person that feels safer with more coverage than the minimum.

There’s really no right or wrong – only the solution that fits YOU. And if you’re a risk-averse person, it might take away any anxiety you experience and hence free up plenty of mental space if you get those “nice-to-have insurances”.

Okay, let’s look at an example to make sure you understood this 4-step process correctly.

Example: Smartphone insurance

Josh bought a new iPhone for $900. The sales clerk tells him that with his purchase he qualified for a discount on a complimentary iPhone insurance: the discounted price is $5 per month. Should he get coverage for his new phone?

Let’s figure it out.

- 1. Is an iPhone insurance mandatory?

Obviously not.

- 2. Could a damage happen?

You bet!

- 3. Could he pay for the damage?

The worst case would be a phone that’s completely broken (- $900). His cash reserve is $3000. So yes, he could pay for it out of his own pocket.

- 4. Does he want to pay for a potential damage?

Since he really takes care of his belongings, bought a waterproof cover including a protective glass, he’s confident that a damage is an unlikely event.

And if it happens anyway, he’s willing to pay for it with his cash reserve. Hence, he decides against insurance.

Obviously, you’re here because you want to insure your hostel. So the question arises: Which are the topics that typically fall under the “must-have insurances” for hostels?

Must-Have Insurances For Hostels

Note that there might be additional mandatory insurances that your country, state, or city wants you to have. Depending upon whether you’re applying for a loan to finance your hostel, the bank might also want you to have additional insurances. This is what you’ll have to find out for yourself.

Hence, the following list contains only insurances for which you have to be active to get covered. Be aware that the actual coverage differs from company to company and from country to country. Hence, this list will only discuss the basics. More on that later.

The must-have insurances for hostels fall into two different categories:

- 1. Liability insurance

- 2. Property insurance (Buildings + Contents)

Let’s start with the former.

#1 Public Liability Insurance Explained

A public liability insurance is typically the most known insurance among people… and for a good reason.

Like the name says, it covers damages that you’re liable for:

- 1. Damages caused by you or your belongings

Example: the man who reads your electricity meter falls on your slippery doorsteps

- 2. Damages caused by your kids (while you met your duty of supervising them)

Example: Your 5-year old daughter lost control over her bicycle and crashed into a parked car

- 3. Damages caused by neglecting action

Example: You see an injured person who needs help but you pretend you haven’t seen anything. After all, you’re late for work

Furthermore, your insurance also covers the costs to defend yourself in cases of unjustified claims (e.g. lawyers and other legal charges).

Typically, a public liability insurance only comes up for damages in your private life. In order to have your hostel insured as well, you either need to pay a premium to include it or you’ll need a separate insurance policy. This depends on the insurance company and plans. More on that later.

The above examples might make you think “Well, that doesn’t sound too bad and I’m not a very clumsy person anyways…”. I partly agree with this when it comes to material damages. However, as soon as humans get injured or even killed, the damage can easily accumulate to hundreds of thousands or even millions.

When this happens, you’re toast. Liability issues can easily put you out of business if you’re not properly insured. No joke.

A public liability insurance covers damages worldwide and should replace them at least up to 10 million dollars. Obviously, it will only come up for damages that you haven’t caused on purpose.

In some states, such insurance is required for running a hostel. However, this is not always the case.

Bottom line:

A public liability insurance is a must-have insurance and is well worth its salt. Even if you have everything in apple-pie order, there’s a high risk of costly damages.

#2 Hostel Buildings Insurance Explained

A buildings insurance is often called a “homeowners” insurance. However, a classic homeowners insurance doesn’t cover damages in your hostel. Hence, “buildings insurance”.

This insurance is often mixed up with contents insurance. For many, the distinction is a blurred one. Let’s fix that.

Imagine you’d lift your entire hostel in the air, turn it upside down and shake it really hard:

- All your belongings that fall out, i.e. are not permanently connected to your building, are covered by your contents insurance.

- Everything that stays, is typically covered by your buildings insurance.

In other words: Your buildings insurance goes hand-in-hand with your contents insurance. They do NOT overlap.

Your buildings insurance protects your hostel building: main structure, walls, outbuildings, gates, and your fixtures.

Covered are:

- Fire damage

- Water damage (through tap water and pipe breaks)

- Some natural catastrophes like storms and hail

That said, the level of coverage varies greatly between different insurance policies. Depending on your actual demand, you’re often able to upgrade your insurance to cover for additional damages (e.g. graffiti damages).

If you’re renting your property, make sure that your landlord has an appropriate insurance. If the terms and conditions don’t cover your hostel business, the insurances will naturally refuse to pay when damages occur.

“Why bother? That’s his problem…” – that’s until he has to kick you out because he is facing bankruptcy. Don’t play with insurance companies. They are ruthless and will not give in just because you didn’t know the consequences.

Lastly, make sure you’re insuring the costs of rebuilding your property rather than the costs of its current market value. Let’s take a look at an example to see what I mean by that.

Example:

Josh buys a hostel property for $500.000 and insures the current market value (= $500.000). 10 years later his hostel almost completely burned down (80% destruction).

When this happens, Josh will receive 80% of the insurance coverage = $400.000.

However, building costs (wages, construction materials, etc.) have climbed during the 10 years by a total of 20%. Hence, he’ll need $480.000 to rebuild his hostel and there’s a gap of $80.000.

To prevent this, simply choose an insurance that covers the rebuilding costs of your property including pollution clean up costs and professional fees.

The actual price of your policy is highly dependent upon the insurance company, how big your building is and what kind of amenities it comes with.

#3 Hostel Contents Insurance Explained

Your contents insurance is the little brother of your buildings insurance. It protects all your belongings inside your hostel: furniture, devices, and other valuables. It even covers food and other commodities.

All this is protected against:

- Fire damage

- Water damage (through tap water and pipe breaks)

- Some natural catastrophes like storms and hail

- Burglary and vandalism

In short: It basically covers the same damages as your buildings insurance plus burglary and vandalism. If your contents get damaged, you’ll get the replacement value (not the market value). That means you could buy the exact same item again without any financial loss.

Again, make sure your policy covers your hostel. A standard insurance will not do the job.

To determine how big the worst-case damage could be, simply sum up all your belongings inside your hostel. Typically, these costs are more than your cash reserve. Hence, it belongs to the “must-have insurance” category.

How Much Does Hostel Insurance Cost?

As a business owner you’re interested in two things:

- 1) What’s in it for you

and

- 2) How much it will cost

Hence, I spare you my bloody-obvious “it depends” and want to give you a deeper understanding of how insurance works.

With this new knowledge, you won’t be surprised to find out that:

- a) Most insurance companies don’t want to insure hostels,

- b) you often have to pay a big premium as a hostel manager due to unknown risk factors, and

- c) you will have to ask for many quotes until you find a proper insurance.

If you belong to the category of nitpickers, you might get offended by how much I’m going to simplify insurance. To set the record straight: this example is not bulletproof and we’re using cowboy maths for illustration purposes.

Perhaps I flatter myself, but I believe that the people who’re able to explain something in a simple manner are the ones who understand it thoroughly.

So here’s how a standard insurance works: All insured people pay a monthly or yearly fee into one pot. The ones that have a legitimate claim during this period will get their damage covered. The ones that didn’t suffer any damage remain unaffected.

By the way: this is one of the main reasons that I dislike insurances. People who have a damage are considered “the lucky ones”. Hence, insurance is almost a motivation to attract damages so that it’s “worth it”.

How truly preposterous is something like this in the context of covering personal injuries? 🙄

Anyway.

Let’s dive into an example to see how the costs are calculated.

Example:

James, Linda, and Emma have chosen an iPhone insurance and pay a yearly fee for it. At the end of the year, James’ phone suffered water damage which is covered by the insurance. Hence, he receives the money for a new iPhone.

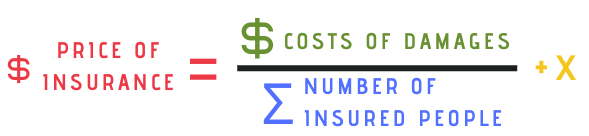

Now imagine you are an insurance company in the example above. How much money do you need to collect from each person in order to NOT suffer any losses?

The answer is ⅓ of the costs of a new iPhone. So how did you come to this conclusion? – Most likely, you’ve just divided the costs of the damage by the number of insured people (3).

Of course, since you and your insurance company have to make a profit from this deal and from taking this risk, plus cover your own costs, you add a certain percentage X to the actual costs.

And that’s basically the entire math behind insurances.

Understanding this simple formula will give you a better sense for all the issues associated with hostel insurances in what follows:

#1 Most insurance companies don’t want to insure hostels

“Why shouldn’t they insure me? Don’t they want my money?!” – you might ask yourself.

Is it really that hard to get coverage as a hostel?

Well, the situation has considerably improved over the past 10 years, but the insurance industry still doesn’t cover all the needs of hostels.

Imagine you’re back in your role as an insurance company. You probably would want a list of all imaginable hazards precisely listed with each and every cost of replacement or repair, right?

And that’s the point of the matter!

- A) Many insurance companies don’t know what a hostel is

You probably wouldn’t insure a Yamaha YZF-R6 when you have no idea what it is and what the typical hazards are, would you?

The same holds true for hostels. What might sound weird is actually true: most people don’t know about hostels. They are just not that commonly known as the following example shows:

P.S. Yamaha YZF-R6 was my last motorcycle. A hell of a lot of fun… and naturally highly dangerous.

- B) There are not that many hostels in the world

There are more than 15600 hostels worldwide. Hence, the database on possible damages is super small compared to other objects like smartphones.

- C) Every hostel is unique

Not one of the 15600 hostels is exactly like the other. Insurance companies on the other hand like to insure things that are standard and uniform (e.g. smartphone).

Insuring something unique is inevitably more time-consuming since you’ll have to make a list of all the hazards (e.g. communal kitchen).

All in all, these three factors make hostels not the most profitable business for insurance companies and also come with higher risks… unless they price a premium which brings me to my next point.

#2 Insurance companies often charge a big premium for hostels

As a consequence of #1, most insurance companies that insure hostels charge an additional premium. This premium covers the additional work of investigating your business and also comes up for the many unknown risk factors.

- High risk → high price

- Low risk → low price

- Unknown risk → HUGE price or NO insurance at all

Oftentimes, they exclude certain aspects of their policy. It’s your job and that of your insurance broker (if you have one) to make sure that all important aspects of your hostel are covered. If there are any discrepancies between what you actually have and what your insurance covers, they might not pay in the event of damage.

Again, insurance companies are relentless and know no mercy.

Additional advice: You can negotiate a cheaper price by presenting the company what measurements you took to reduce or prevent potential threats.

This could be the installation of smoke alarm systems, providing fire extinguishers, adding emergency lighting, installing a keycard entry system, etc.

#3 You will have to ask for many quotes to find a proper insurance policy

When researching insurances you definitely have to shop around to get a good deal. And yes, this will take some time. There’s no way around that.

However, keep in mind the consequences of not having insurance. This “simple” step can prevent you from having to sell everything you own and will own in the future. It’s well worth the effort.

Luckily, there are professionals who’ve studied the topic and can help you out. Let’s explore who they are and what they can do for you.

Where To Get Hostel Insurance

Knowing what kind of insurance professionals there are and what their interests are is the first step towards getting coverage for your hostel.

Insurance Agent vs. Insurance Broker

In simple terms, insurance agents typically represent one insurance company. Hence, they can offer you only one solution (“the best”) for your problem.

Sometimes, but rarely, this is really the best option out there. However, the likelihood isn’t very high. It can also be the case that they don’t offer the kind of product you need.

Typically the “worst form” of insurance agents are the ones working in a multi-level marketing scheme, aka pyramid scheme. In its simplest form, this means that the person on top of the other person participates in their sales.

Hence, the ones at the very bottom deal with a lot of pressure to sell their products in order to meet their requested numbers – often to the disfavor of their customers’ interests.

You might have experienced this scheme yourself: this is when an old friend from high school suddenly calls you and is interested in helping you in your finances… #micdrop

That said, back when I was running my own financial consulting business, I was appalled by the kind of greedy insurance people who only make the sale for their own benefit.

Let me get this straight:

There are A HELL OF A LOT of black sheep in the finance industry

There’s a reason why this industry has such a bad reputation. It’s reputation is hard-earned and its reps apparently fight tooth and nail to keep it that way.

If I learned one thing from working in the finance industry, it’s this sad truth.

BUT there are also a few good-hearted, knowledgeable and upright people out there who have your interests at heart!

Hence, not all people working in a multi-level marketing scheme are per se “bad”. But the likelihood of finding genuine people is way smaller compared to an insurance broker.

After all, by being a representative of only one company, they chose to limit their options regarding how well they can address your specific situation.

Simply put, insurance brokers are the “premium version” of insurance agents. They typically work with multiple insurance companies to ensure they can compare different quotes. All that is being done to offer you the one that fits best to you and your individual needs.

This model comes with the benefit that you have one person to talk to for all your policies instead of five different people for each insurance policy you need.

A special form of insurance brokers are the ones that are “independent”. That means they’re completely free in their choice of the insurance company. Hence, the likelihood of you getting the true best offer is highest.

However, not everyone who claims to be independent is really free in his decision-making. Sometimes they work with just a couple of insurance companies and call themselves broker for that reason.

This is something you should actively ask for in your first consultation! Let him or her show you a certificate or other evidence that tells you the truth. If they get nervous you probably want to look out for another broker.

Back when I had my own financial consulting business in Germany, it was compulsory to be registered online and display to which “category” of consultant you belong. Hence, all my clients could instantly see that I was completely free in what I offered them.

No matter where you end up, make sure you know exactly which insurances you need and want BEFORE your first consultation. Otherwise, you’ll likely end up with many more products and extent of coverage than you really need.

Insurance agents and brokers are often excellent sales people. They’ve studied human psychology and know exactly which strings to pull and what phrases to use to make the puppet dance.

What looks like they say on the fly was studied and rehearsed a hundred times. Each joke, each break is part of the script. Every objection was investigated to quash it. And even if you ask uncommon questions, they have plenty of techniques to get you back on their track. All leading to the signature that they want from you.

Why do I want to reiterate that so much? – I’ve been there. I’ve seen it.

Now, is any high-volume sales person acting in an unethical manner? Definitely not. But I guess that’s a topic for another blog post 😉

Finally, how do they get paid?

Typically they receive a commission that is a percentage of the overall price you pay. No one will tell you exactly how much this is. However, it’s already included in the price and you typically don’t pay any extra money.

Some insurance brokers want to get paid by the hour instead of a commission. The advantage is that there are no conflicts of interest. That said, if you find an ethical insurance broker paid on a commission model, you can definitely save a good amount of money.

Bottom line:

Search for an ethical and independent insurance broker that has experience with hostels.

I recommend you have a consultation with several insurance brokers to find one with experience and with whom your gut feeling is “right”. I also advocate you steer away from multi-level insurance companies.

Other Options

Besides asking for help, I recommend you do your own research and be proactive yourself. The better informed you are the more likely it is to get a good insurance policy.

Also, note that even independent insurance brokers are not able to represent every single company. Some insurance companies simply don’t work with agents or brokers.

Here’s another option that did wonders for other hostel owners:

- Ask other innkeepers in the area about their insurances

But always take their advice with a grain of salt! After reading this blog post, you probably already know more than 95% of them about insurances and their practises.

Not all will be willing to help you but that’s okay. As a business owner, you want to adopt the mindset of a boxer: It’s not about how many hits you make – what matters is how many hits you can take and still keep pushing forward.

What about online comparison websites?

Well, they are great for private standard insurances (e.g. smartphone, car, etc.). However, you probably won’t find any comparison sites for hostels since the prices and conditions are tailored towards your individual hostel.

Lastly, if you choose to work with an insurance broker, ask him to prepare 3x different options for each insurance so that you can choose yourself.

Some people recommend to work with several insurance brokers and be in direct contact with insurance companies to get as many offers as humanly possible in order to price them out against each other.

Technically, this absolutely works! So yes, you will probably get the “best” offer doing that.

However, if a broker really went above and beyond for you and answered all of your questions, I personally think it’s only fair to stick to him respectively her – even if that offer costs you $20 more per year. Remember that he or she might be there to answer future questions as well.

In Germany we have a saying: Live and let live.

Keep that in mind.

Where to find suitable insurance companies?

Simply google for “hostel insurance [your country]”. Easy as that.

I don’t want to recommend any specific companies because my experiences are based on German insurance companies and not specifically in the context of hostels.

P.S. People who read this guide were also interested in my article about whether to buy or lease a hostel property.

DISCLAIMER: The above information is for informational and educational purposes only. It does not constitute financial or legal advice and does not establish any kind of financial-client relationship with me. The information provided has been prepared without taking into account your objectives, financial situation or needs. Before acting on the advice, you should consider its appropriateness for your situation. I am not liable or responsible for any damages resulting from or related to your use of this information. Read my full disclaimer here.

STOP! 🤚

Before you leave: Answer this quick question and help our community.

Which INSURANCE COMPANY (1) did you end up with for WHICH POLICY (2) in WHICH COUNTRY (3)?

Share your opinion in the comment section below!

All three recommended insurances + car insurance for hostel van.

Buildings insurance is covered by our landlord though.

Cheers, Norma

Thanks for sharing, Norma 🙂

Loooove you !!

Super informative!

I read your post about the business plan before – great work!! 😊

Thanks Amanda! 🙂

I appreciate your feedback.

The story with the friend of high school happened to me twice !!

Suddenly your old mates (who you haven’t heard from in years) want to help you with your investments and insurances……. so sick.

Well, sad but true.

Public liability + building insurance

I don’t see the point of paying for contents insurance since we don’t really have that expensive equipment in our hostel.

But the others are really a must in my opinion.

Thanks for sharing 🙂

Am I the only one who feels bad for having a smartphone insurance?! 🤔😅

Haha 😄

I’m sorry.

I contacted 8 companies so far … and 8 times I got rejected. This sux.

Hi Georg,

you might have more luck to contact an independent insurance broker.

They typically have many connections with other companies.

Hope that helps.

We do not have any insurance except the ones that are mandatory. I just don’t trust these folks. However, we do have a quiet big cash reserve in case anything severe happens.

Hi Angela,

thanks for sharing your opinion.

I don’t necessarily agree with it though. I think it would be better to invest a “huge cash reserve” in other assets to earn interest.

However, there’s no right or wrong – there’s only the solution that fits you!

When we applied for a loan, banks wanted us to have building insurance and the same insurance company also offered a contents insurance which was cheaper if you decided to take both at the same time. So we chose the combo.

Hi Clyde,

thanks for sharing your experiences.

That’s interesting to know.